Tony was a guest speaker at the New Zealand Property Investors Federation Conference 2019 which was held in Rotorua. This is a

summary of what he spoke about which has been provided by him.

My aim to help Kiwis make better decisions for their businesses, investments, home purchases, and people by writing in an easy to understand

manner.

EVERYTHING IS GREAT If you take a look at the data, you’d conclude fairly quickly that people in New Zealand must be

feeling really happy about the economy.

The unemployment rate sits at 3.9% compared with 5.3% in Australia, and job numbers have risen by almost 400,000, or 17%, in the past five

years.

The economy has recorded positive growth for 34 quarters in a row and increased in size by 17% from 2014. Real income per capita is 16%

higher than before the global financial crisis.

The volume of retail buying we each do on average is 21% higher than pre-GFC.

The number of dwellings being built is the highest since 1974 and 50% above the average yearly number for the past 20 years.

Export receipts have risen about 5% in the past year.

The terms of trade (export prices versus import prices) are only just below a record level.

The inflation rate is only 1.5%.

The government has completed its fifth year of surpluses.

The current account deficit is only 3.6% the size of the economy.

The number of people visiting New Zealand is 40% higher than five years ago. Mortgage interest rates are the lowest in half a century and

still falling.

The Kiwi dollar on average is 5% below its average for the past decade.

But there is little ecstasy out there. Instead we have the following.

The ANZ Business Outlook Survey shows a net 54% of businesses are pessimistic about the economy. This is down from a net 18% positive just

ahead of the late-2017 general election and the worst reading since 2008. A net 76% of farmers are pessimistic, the worst reading since

2006 despite export prices in NZ dollar terms rising 70%. Construction sentiment at -55% is consistent with pessimism levels just after the

1987 crash.

A net 9% of businesses plan cutting investment versus a ten-year average net 9% usually planning to raise capital expenditure.

Consumer confidence measured by Roy Morgan and ANZ sits at a reading of 114 which is below the 120 ten-year average and the weakest since

2015.

WHY THE WOE We can consolidate the numerous factors people can cite into five broad categories plus a bunch of

miscellaneous items

A Slowdown Has Happened

The latest economic growth rate for NZ is 2.4% in the year to June. This is a slowdown from an average 3.5% achieved between 2014 and 2018.

That earlier surge was caused by three key factors.

A 40% rise in tourist numbers.

A strong rise in residential construction.

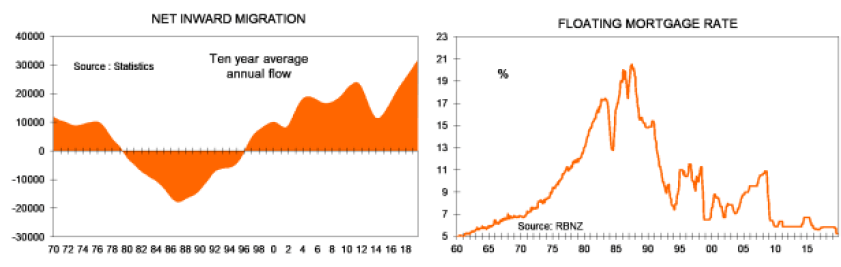

A net migration boom adding 4.5% to the population (some 230,000-extra people).

In addition, oil prices fell sharply over 2014-15, interest rates fell away from 2015, export prices rose, and there was underlying growth

in sectors like aged care, healthcare, and the digital economy.

But now visitor numbers have flattened out, net migration has eased to near 50,000 the past year from a peak 64,000 three years ago,

businesses have become wary of the new government and almost stopped growth in capital spending, and the economy lacks capacity.

Labour Force Management

The old days of high unemployment and employers being able to place an ad in the newspaper and sort the wheat from the chaff from

motivated, skilled applicants has gone. The availability of all types of labour has plummeted, not just in New Zealand but around the world

– especially in the construction sector after the GFC led people to abandon building careers.

A net 42% of NZ businesses say they are finding it difficult to source skilled labour. This is down from the tightness of mid-2018 but well

above the average reading of 30% difficulty. A net 28% of businesses say they find it hard to get unskilled people. The average is just 8%.

What is interesting is that the gap between difficulties finding skilled and unskilled people is very small. So even the option of hiring

people to train up is difficult.

But the problem of labour force management is more than just an overall volume and relatively high shortage of unskilled people situation.

We are now over ten years down the track from the GFC ending. Many hard-working, loyal people have refrained from shifting jobs or asking

for decent pay rises because of worries about the world economy. Now these people can see that there are plenty of opportunities. They have

been burdened with repeatedly training up unmotivated lowly skilled people and apologising to customers for the poor-quality work which

increasingly is occurring.

The skilled loyal people are starting to leave and this costs businesses dearly as these people are taking their “meta-knowledge” with

them. This is knowledge not just of how processes work in a firm, but how things go wrong and the early signs of problems developing. Their

knowledge can lead to problems being captured early. Loss of these people can mean problems escalate and businesses who are already losing

money by having to redo work will see losses grow even larger.

The low availability of labour is blindsiding many Kiwi businesspeople who are used to being able to source employees easily and to set the

rules of engagement. And an extra problem they have is that Baby Boomers are increasingly retiring and more and more employees are younger

people requiring different management skills because of their different expectations. Plus, a key labour problem around the world is that

the high speed of change is rendering skills obsolete at the fastest pace ever seen. The need for intensive retraining programs has grown,

but businesses focussed on cost-cutting are not doing enough people retooling. And lack of investment is curtailing productivity growth on

top of that caused by government regulations surrounding the likes of health and safety etc.

The answer for businesses in this environment is to stop focussing primarily on profit growth via attempted output growth. Targeting higher

output in a capacity-constrained economy can be very costly. What some businesses need to do is cut output. Cut loss-making and low profit

customers, locations, and product lines. Develop growth plans first by working out the quantity and quality of resources which can be

employed in coming years, then figuring out what output growth that will allow.

Pricing Power Decimated Between 2005 and 2007 New Zealand’s labour market was very tight and one of my main

messages back then, along with handling the lack of labour by cutting output, was to raise prices to both boost profit and ration output.

Many companies did so quite successfully, hence rising inflation then rapidly rising interest rates.

But these days businesses in most industries have lost the ability to comfortably raise selling prices and get away with it. In the old

days it cost consumers and business input buyers a lot to find alternatives to products they were buying. Shoppers had to spend time,

petrol, and generate stress driving around town finding shops hopefully selling the item they had discovered cost more than they expected

in their usual location.

But now, courtesy of the internet, it costs nothing to go online and search for alternatives. In fact, looking for stuff online is a

recreational activity and undertaking product searching is fun. So, faced with higher than expected prices consumers now do not

automatically pay. They go online and possibly also write something negative about the original retailer on social media.

The power of most businesses to raise prices has been permanently reduced by the internet. This is one key explanation for sustained low

inflation around the world despite firm economic growth and resource shortages.

The solution for businesses is to focus on clients, products, and locations where they may have some pricing power, and again to drop

low-profit things. Cutting costs through automation, relocation, reconfiguration is also necessary.

Social Licence to Operate Challenged In August in the United States, 180 of the country’s largest businesses

said they are changing their primary focus away from maximising shareholder returns to acting for the benefit equally of shareholders,

customers, staff, suppliers, and the community. This is a substantial change and a key driving force behind it is the increasing societal

concern about businesses and their impact on society.

In the United States there are concerns about businesses creating and promoting the opioid addiction epidemic. In many countries there is

disgust at high executive salaries and payment of bonuses even when companies perform poorly, as happened in banking sectors following the

GFC, and Fonterra in NZ.

There are growing concerns about plastics and plastic packaging in particular. Some massive businesses are playing loose with people’s

personal data and privacy. Worries about climate change escalate every month. Wages growth has failed to keep pace with profit growth in

most countries, and in some sectors worries about water pollution are becoming dominant. Gender diversity and inclusiveness are new large

concerns.

Pressure on businesses to change the way they operate are coming from governments via regulations, millennial staff, clicktivists, and

managed fund operators.

Businesses are having to spend more time mitigating the negative impacts of their activities on the society. Operators in some sectors feel

disrespected and dismissed – farmers – while others – tourism operators – face an existential threat should the world take climate change

seriously and cease travelling huge distances to see smaller versions of landscapes already available to them for virtually no air

travel.

In a nutshell, running a business is no longer just an issue of making something and selling it for more than it costs to produce, and

around the world business operators are struggling to identify often quickly appearing areas of societal concern, and adapting to them.

Offshore Problems It is true that anyone who has focussed just on offshore problems this past decade and

refrained from investing, hiring people, or buying a house, has probably missed out on substantial gains and profits. Offshore worries

about the likes of the Euro falling apart or Greece going bankrupt have by and large been red herrings.

But world growth is now slowing and some of the offshore factors in play do have capacity to go bad and affect us here.

US-China trade war

Because almost everything we export from NZ is made in NZ we are not seeing the massive disruption to manufacturing globally from US

businesses looking to source inputs outside of China. But we are vulnerable to any generalised movement away from multilateral trade rules

and relationships, and shifts in sourcing of primary products perhaps as part of any resolved US-China trade deal.

China Growth

The pace of growth in China has already slowed from the four-decade average of 8.1% p.a. to almost only 6%. Further slowing is likely and

this means a reduced pace of growth in demand for our primary products, especially as China may use market access as a weapon against

countries not kowtowing to certain demands. 29% of our export receipts come from China, (15% Australia) Chinese visitors spend about $1.6bn

p.a. in NZ, and Chinese students make up about one-third of our export education sector.

Middle East Tensions

It is hard to know what is new and what is just ongoing friction. But there is potential for disruption to oil supplies which history shows

will affect our growth and world growth and sentiment.

Sharemarkets

Prices are very high and although the scramble for yield is continuing as the global consensus settles around low interest rates for

longer, there is potential for a market correction of large magnitude if enough investors decide to take risk off the table and bank

multi-year capital gains at the same time.

European Growth

Germany may be in recession, Italy possibly also. Doubts about the cohesion of the EU and Euro persist.

Brexit

No-one knows how things will pan out and potential for disruption remains very high.

Miscellaneous Concerns This is a non-exhaustive list of other things potentially causing concerns in the

business sector and maybe amongst consumers as well.

NZ population growth has slowed down recently courtesy of easing net migration inflows and the aging population.

Credit availability structurally declined in and following the GFC and further decline is likely as the Reserve Bank looks set to raise

minimum bank capital requirements. Banks will react by restricting lending to sectors requiring higher capital to be set aside than for low

risk sectors. That is, they will reduce lending to farming and commercial property developments and favour buying of existing houses.

The infrastructure pipeline looks fragmented. Gaps between big projects mean skilled people may shift offshore to work on other projects

and firms may also relocate machinery or not invest in new equipment.

There is not confidence that the coalition government has the ability to respond should the world economy weaken sharply. The ideological

drivers of some parties and MPs is seen as blinding them to business pressures and requirements and there are growing concerns that should

Labour and the Greens get re-elected, the current pressure being placed on sectors such as farming would intensify – especially if NZ First

is not in the next government.

Monetary policy easing in recent years has taken interest rates to such low levels, and money printing offshore has proven so ineffective

in stimulating lending/borrowing, growth and inflation, that should a shock downturn come along, the ability of our central bank and others

to effectively combat it as in the past three decades would be minimal. The speed of change in our personal lives, business operating

environments, and maybe our societies and planet are the fastest we have ever seen. Potential for disruption to so much of what we do can

easily lie just around the corner.

Retirees and those approaching retirement face an environment of extremely low returns on low risk assets. Their logical response will be

to spend less.

New, big offshore retailers are set to enter NZ with potential severe disruption for some retailers, and some are already here. Costco

Wholesale, Ikea, Chemist Warehouse.

SO ARE WE MUNTED No. As humans our natural tendency is to focus on the negatives. We are more attuned to threats than

opportunities. Those who ignored threats in the past got eaten by the wild animals and weeded out of the gene pool. We are the descendants

of the scared and cautious cowards who ran for their caves at the first hints of trouble. So, we are naturally drawn to negative headlines

and peddlers of woe on the internet.

There are some strong forces suggesting that the slowing of NZ growth since the first half of 2018 will not continue in straight-line

fashion to recession – unless the world economy falls over and that is not likely despite the gasps of astonishment about President Trump

or the UK Prime Minister, or leaders Bolsanaro, Duterte, Putin, Erdogan, el-Sisi, Maduro, Xi, Trudeau, Kim, and so on.

Net migration inflows have eased from 64,000 in mid-2016. But at rates just over 50,000 there is still an extra 1% boost to our population

occurring. That does not lift income per capita, but that is not relevant for businesses simply hoping for more customers.

Consumer confidence is below average but still in positive territory.

There remains underlying growth in sectors like aged care, healthcare, and the digital economy.

There is so much construction to be done yet a shortage of people to do the work, that activity levels in the widely defined construction

sector are likely to remain firm for many years.

World growth is expected to recover slightly next year.

Monetary policies are being eased around the world, and while their effectiveness has reduced, the changes nonetheless will deliver some

small stimulus.

The NZ dollar is below average and may decline further in the near future.

Our terms of trade are only just off record highs.

Fiscal policy is on a stimulatory setting and highly likely to be eased further before and after next year’s general election.

The tight labour market is keeping job security firm and buffering the economy.

It seems reasonable to keep expecting that outside of unpredictable shocks, our economy will continue to record growth rates near 2% - 2.5%

over the next 3-5 years, that inflation and interest rates will remain low, and that wages growth will be mild.

However, in some sense it does not matter all that much for many businesses just how fast our economy grows in the near future. That is

because their problems are not solely related to not being able to find customers to service, but to shortages of resources, rising

compliance costs, rising rents, and shrinking margins.

In some sectors such as construction, retailing, and farming, we are seeing businesses fail in spite of strong sectoral fundamentals. This

tendency for the most indebted, disorganised, and optimistic to be weeded out is likely to spread to virtually every other sector in the

economy over the next three years. A period of weeding out is upon us – and that weeding out may become quite severe if the world economy

turns down sharply and/or our commodity export prices collapse.

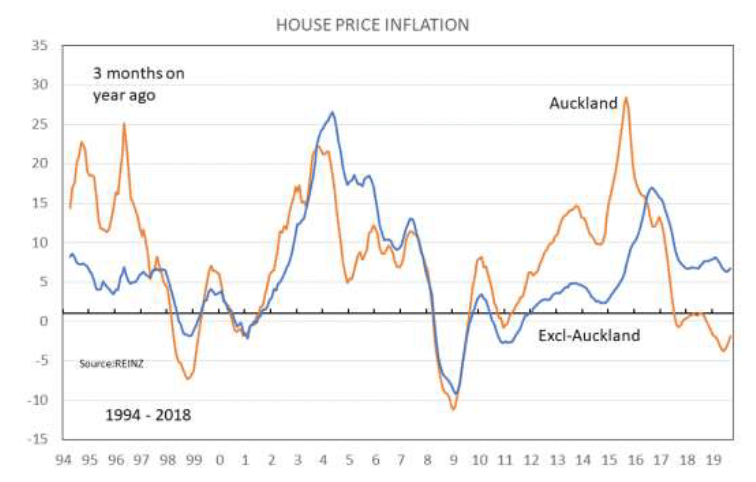

HOUSING Between 2011 and 2016 Auckland house prices doubled on average. Since the middle of 2014 prices on average in

the regions outside of Auckland have gone up by 56%. Why have prices surged so much? It is certainly not because there has been a huge

lending splurge from the banks. Over the past five years the level of household debt has risen by 39%. This is not much above growth in the

nominal size of our economy of 27%.

In the previous five years ending in 2014 housing debt grew by just 18%. In the five years to 2019 debt grew 70% and in the five years to

2004 68%. It was pre-GFC (Global Financial Crisis) that debt surged, not since then.

The surge in house prices reflects a large number of factors altering, some over a very extended period of time.

Two income families from the 1970s.

Structural falls in interest rates 1992, post-GFC.

A structural rise in credit availability from 1985.

Bigger houses being built now vs. the past.

Tougher building standards, fees etc.

3-decade message to invest for retirement.

Foreign buyers.

Population shifts to

Older couples divorcing.

Net migration flows shifting.

Airbnb

Land supply constraints.

The most recent surge we can attribute substantially to under-building of houses in Auckland ahead of the GFC, the structural decline in

interest rates, a surge in net migration inflows from 2012, and buyers catching up after delaying purchasing for various reasons from 2007 –

2011. FOMO – fear of missing out – also kicked in strongly once Auckland got rolling.

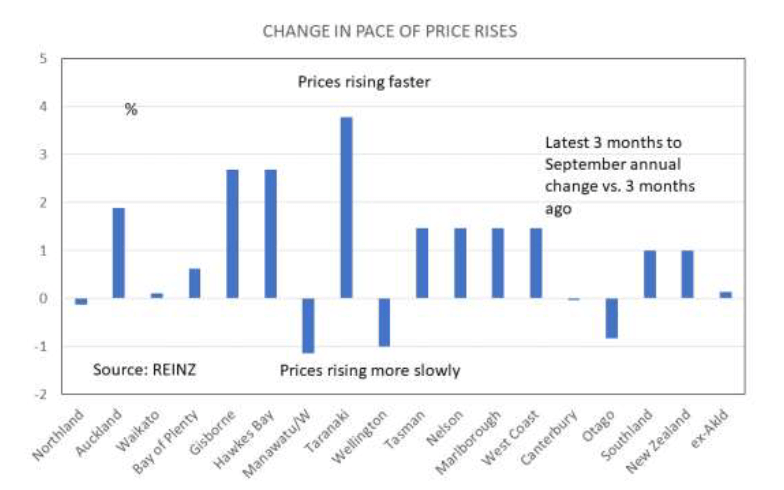

The most recent data released by REINZ on October 15 tell us that listings remain in relatively short supply, that turnover is showing

signs of slight improvement in Auckland, and that prices now appear to be rising anew in Auckland while continuing their firm gains in most

other locations. I produce graphs and commentary around regularly released data in my weekly publication “Tony’s View” available for free

from www.tonyalexander.nz and by emailing me asking to subscribe at tonyalexander5@outlook.com

So what lies ahead? Is it reasonable for instance to think that our markets will undertake a recovery such as that which is happening in

some of Australia’s state capitals? I discuss this issue in my October 17 Tony’s View, but in summary, we did not follow Australia’s 10% -

15% house price falls for reasons such as these which gave special downward impetus to Australia’s markets.

Post-GFC in Australia substantial irresponsible lending with poor repayment ability assessment was undertaken and about three years ago the

Reserve Bank of Australia tightened rules on lending to investors to prevent this. In NZ we did not have the same loosening of lending

criteria for investors post-GFC.

In Australia about 60% of dwellings built are apartments and this market can be highly volatile. In New Zealand only some 12% are

apartments.

More Chinese were active in Australia’s markets than New Zealand’s. So when rules were tightened in China to more heavily restrict capital

outflows some five years ago the impact was greater in Australia than here.

In Australia people started using their Self-Managed Superannuation Funds to gear into property. Banks stopped lending for this purpose a

couple of years back, taking away a source of demand.

States in Australia over the past two years have introduced and raised taxes on foreign buyers and owners of residential property.

Australia generally has an over-supply of dwellings whereas in NZ we have shortages.

Australia’s markets fell away but ours did not. Now, in the space of just four months the question people ask me has shifted from whether

we will follow Australia down to whether we will follow them strongly up. We will not for the following reasons specific to Australia.

Interest rates have been cut three times so far this year.

Rules on bank lending to investors have been eased.

A big court case against Westpac alleging improper calculation of debt servicing ability was thrown out.

Investors are catching up on buying after pulling back.

A fresh wave of owner-occupier buyers has entered the market sensing that there is an opportunity to pick up something well-priced

following 10%+ falls in properties.

Hefty publicity is being given to the recent surge in prices with elements of FOMO likely to now be in play once again.

Nonetheless, can we reasonably feel that the worst for Auckland (prices down 3.5%) is over, and that the regions may retain more strength

than earlier thought? Yes.

There is extra support for housing now coming from investors partly reacting to the confirmation of no capital gains tax. But I give that

factor only a small weighting. Instead, the new decline in term deposit rates and expectations of further declines is encouraging investors

who were thinking of selling to hold onto their properties. And others who may have felt no desire to purchase property in the near future

are also searching for yield and perhaps choosing to place their funds into a property investment of some sort.

Factors supporting our housing market going forward then amount to these.

Net migration inflows are holding up well near 50,000 per annum, and given slowing world growth it seems reasonable to expect that our

population growth rate will remain supported from this source for many more years.

Interest rates are low and going lower.

The economy looks likely to continue to comfortably support a strong labour market. Good job security and rising job numbers are supportive

of housing.

There is little prospect that the centre-left government will look for new ways to penalise landlords. However, introduction of

ring-fencing of losses and higher rental property standards may encourage some investors to sell.

Housing supply is rising but limitations on the availability of labour suggest a construction boom is not going to happen.

Having said that, the rise in house supply is likely to constrain feelings of FOMO in Auckland. And for that reason, while it now seems

reasonable to expect price gains close to and even above 5% for each of the next three years, it would be optimistic to anticipate gains

approaching and exceeding 10% per annum. I am not willing to say that Auckland is starting a new cyclical upturn.

In the regions low interest rates are comfortably extending a period of catch-up price gains which I had expected to be near complete by

now. But to anticipate a fresh price surge when there are some specific factors hitting the pace of growth in regional economies – a

dairying “downturn” driven by environmental concerns, and near cessation of growth in tourist numbers – would be unrealistic.

Now and then I produce graphs for each region showing how prices compare with long-term averages and they appear in Tony’s View.

IMPLICATIONS

Businesses It’s only going to get harder to run one’s business. Consider running a one-day Strategic

Planning session and give thought to the following.

How to keep up to date with the increasingly rapid speed of change in consumer preferences and shopping methods, distribution chain

changes, products from competitors and so on. Extra investment may be needed in real-time data services showing sales and marketplace

changes. Extra attendance at conferences may be needed. Collaboration with researchers etc.

Skills are becoming harder to source and become obsolete more quickly. Consider how to retain and retrain staff, and how to train up new

people quickly. Consider the remuneration and work flexibility desired by new workforce entrants and older people wanting or needing to

stay in the workforce but not prepared to wok as much as in the past.

Look at Statistics New Zealand sub-national population projections to get a feel for where customer base growth may be strong and where

weak. This can guide decisions on locating facilities and targeting markets. Consider the strong growth in cities and how that is where the

future workforce will come from – not the countryside which is increasingly reliant on migrants to fill farm jobs.

How to reduce use of plastics and cut greenhouse gas emissions. How can you prove environmental sustainability to your customers?

Interest rates look set to remain low. Do you need to pay for specialised interest rate risk management advice?

Banks are likely to have to hold more capital in coming years and willingness to lend to businesses generally will decline, especially for

agricultural operators and commercial property developers. Before planning to grow consider not just what labour resource you can command

going forward, but what level of bank funding will be available. You will likely need to shift toward financing growth through new capital

and retained earnings.

You might be fine, but your vulnerability could be to your product and service suppliers. Their work chain interruptions may cost you

dearly in failing to meet your customer requirements and expectations. Maybe consider higher inventories and back-up service providers.

Margin management has become permanently more difficult. Raise prices where you can, but cut back reliance on low-yielding goods and

services, customers and locations.

Be aware of special political risks which come from selling into China and bias output plans toward other markets.

The population is aging yet at the same time more migrants are coming in. How are these trends relevant for your products and customer

base, and for staffing?

How vulnerable are your premises to increased inundation risk from global warming in terms not just of physical impacts but asset repricing

and insurance availability?

Investors Generally There has been a structural downward shift in global and local inflation in recent years

along with the strength of the linkages between the pace of economic growth, relative shortages of resources, and the resulting upward

pressure on prices. This has produced a structural downward shift in the average level of interest rates whether measured by government

bond yields, central bank lending and deposit rates, mortgage rates, corporate bond rates etc.

Because of reduced returns on low-risk interest rate products investors have sought other investments. This has pushed up the prices of

assets like property and equities and structurally reduced their yields as well.

For investors, the permanent lowering of interest rates has permanently lowered returns on all products. Thus, the starting point for

anyone contemplating their investments going forward has to be an explicit acknowledgement that one cannot achieve the same nominal or real

returns as in the past – unless one takes on more risk.

And that is the kicker to be wary of. Higher returns have almost always required higher risks. But history shows us that our individual

ability to understand the nature, extent, and driving forces behind the higher risks we take on is often much too low. Partly this is

explained by the fact that for most of us investing is a stressful activity and our brains want that stress taken away. So, we tend to too

quickly latch onto investment products which offer the good returns we want and maybe feel we deserve, without taking the time to properly

understand the risks to returns along the way and the capital value and tradability of our investments and how these things can change.

If investors can become aware of this human tendency to skip over the details then greater effort can be out into understanding something

before investing in it. And that can mean greater understanding of what is happening if and when returns fall for a while, and that in turn

can reduce not just the stress at such times but the risk of panicked selling. This panicked selling is again something driven by our

brains trying to avoid stress.

We tend to over-extrapolate the most recent things we see. So, if an asset falls in price our natural inclination is to believe that it

will fall in price further. Our focus then shifts away from the long-term plans and expectations we had when we made the investment toward

avoiding what we now believe will be further losses. We will crystallise our loss to date in order to avoid future losses.

People like Warren Buffett and skilled fund managers know we think and act like this and they become contrarian buyers – picking up

cheapening assets in times of panicked selling because the long-term fundamentals underpinning them may not have changed at all.

So, as investors contemplate what to do with their funds now that low risk returns on assets like bank deposits are so low, and that share

prices and many property prices have already structurally adjusted much higher, they first need to understand their own psychological

weaknesses and behaviours regarding investment decisions. Do that and then assess the range of assets on offer in more dispassionate

manner.

This publication is written by Tony Alexander, independent economist.

This publication has been provided for general information only. Although every effort has been made to ensure this publication is

accurate the contents should not be relied upon or used as a basis for entering into any products described in this publication. To the

extent that any information or recommendations in this publication constitute financial advice, they do not take into account any person’s

particular financial situation or goals. We strongly recommend readers seek independent legal/financial advice prior to acting in relation

to any of the matters discussed in this publication. No person involved in this publication accepts any liability for any loss or damage

whatsoever which may directly or indirectly.

So what deals do you find? Well pull up a chair because we find a lot of very different properties for our wonderful clients, who (probably to their surprise) don't all want the same thing!

Read More…

.jpg)