Most investors are familiar with the saying, "You make your profit when you buy." So how do you consistently do this? There are a two very common schools of thought; firstly, to buy properties with high yield and secondly to purchase the worst house in the best street (or suburb). Both can be true, however, often properties chosen for high yield or for their good area alone under perform in either cashflow or capital gains, or sometimes even both.

Experienced investors select property based on their determination of "true value" at time of purchase. Mastering this art will enable you to make profitable buying decisions every time.

So what is True Value? True value is market value plus or minus an adjustment for potential and for risk. Market Value would be the expected sale price between a willing seller and a willing buyer. The True Value however, factors in a discount or a premium, caused by the imperfections of the property market.

These factors can be obvious, like a property that has been neglected or one with bad tenants refusing access. These factors can also be hidden, for example; planned infrastructure in an area, ability to subdivide, high vendor motivation and economic market cycles. If the True Value is higher than the Market Value then the property is likely a good investment. However, if the True Value is lower than the Market Value then it is likely not a good investment.

Sophisticated investors do not seek to "steal" properties to make a profit. They identify the True Value, purchase properties at close to Market Value - and still make extra-ordinary profits.

It is important to note that yield is not the most important factor in identifying True Value. Yield is essentially a measure of risk.

Higher yield equals higher risk: risk of tenant damage, risk of vacancy, risk of neighbours causing problems etc. Every investor should be

able to make a yield calculation very quickly, so I won't discuss how to do that here. It is common though for investors to compare a

property returning say 4.5% with one returning say 4% and conclude that the first property is "better value." While this is

sometimes the case, it is often also a false conclusion.

Let's look at two $500,000 properties; one with a 4% yield and one with a 4.5% yield. There is an annual cashflow difference of $2,500.

However, this amount would pale in comparison to the tens of thousands of dollars that could be created or lost by the property's

"hidden potential" or "hidden costs (risks)" More on this later.

It is also important to note that when choosing an area to invest in, growth potential of that area is far more important than the property

being in a "good area". Traditionally, we are taught to buy in good areas for capital gains. However, a portfolio made up of

properties in below average but up and coming suburbs will have superior cashflow AND capital gains than a portfolio of properties held only

in more expensive suburbs.

So, if not by yield or good area, how do investors identify True Value and make profitable buying decisions? The steps to determine True

Value start with identifying the Market Value of a property and then making an adjustment for the hidden potential and the hidden risks of

the deal so let's look at how to determine Market Value.

How to determine Market Value

Market Value is obtained by looking at recent sales in the area and then comparing whether those properties are superior or inferior to your property. If your property is inferior, then the Market Value is less than the comparative sale. If it is superior then the Market Value is more than the comparative sale. Doing this across a number of recent sales allows you to accurately determine a property's Market Value.

To increase your chances of finding properties being sold for less than Market Value, look for highly motivated vendors, poor marketing, a poor real estate agent, untidy properties etc. As you look at more properties, a good deal stands out so much that you will have no doubt whatsoever that it is an excellent value proposition. In this case, be speedy. If a trusted agent calls you, then turn up immediately with your cheque book to secure that deal.

Once you know the fair Market Value of a property you then need to make an adjustment to get True Value. The following list is not meant to be a comprehensive but rather some factors to consider that will influence that adjustment.

Determining True Value: Adjust UP for hidden potential

Development potential - If you know that the council would allow subdivision or you can build a minor dwelling, add an extra room, convert the garage etc then increase True Value up.

Renovation potential - If the property is run down and in need of renovation then the market value will likely reflect more than the cost of doing that renovation. If the renovation costs $40,000 you might be able to increase the value of the property by $80,000 so even if you plan just to rent it out adjust True Value up.

Ability to increase rent - If there is the possibility of increasing rent by adding a sleepout, adding an extra room or simply that you know rents are increasing rapidly in a certain area then adjust True Value up.

Large land size - Another reason not to look at yield alone is that the property may be on large land. Even if you are not able to subdivide right now and that may not be your game anyway, you will likely receive disproportionate gains in the value of the property so adjust True Value up. (Please consult with your tax professional if investing in land with the view of subdividing).

High liquidity - Any property that is in a nice "leafy" area and is attracting proportionately increasing population and will appeal to a high group of end buyers, especially home buyers means that you will likely get a higher price when you finally come to sell so adjust True Value up.

Perceived poor areas - If the press or even another investor holds a prejudice or a preconception about a certain area it is likely that you can adjust True Value up.

Infrastructure - If you are privy to knowledge of a new train station, new road, expansion of factories or new malls this will increase the value of surrounding properties disproportionately so adjust True Value up.

Replacement cost - If you know that inflation and or replacement costs are outstripping purchase costs then you can confidently adjust True Value of all property up.

Market recessions - This is a biggie. Every eight to ten years we experience an economic recession during which time the mass media is particularly pessimistic, the banks don't want to lend, unemployment increases and property prices drop. In a market recession adjust True Value up.

Sophisticated investors do not seek to "steal" properties to make a profit. They identify the True Value, purchase properties at close to Market Value - and still make extra-ordinary profits.

Determining True Value: Adjust DOWN for hidden costs (risks)

Expenses - Investors must be very careful to identify all expenses especially those which an investor has no control over such as body corporate fees and leasehold fees. For cheaper properties which obviously attract low rent the cost of fixed chattels etc does not change. A stove costs the same to replace anywhere in NZ but takes a lot longer to pay off at $250/week as opposed to $500/week so adjust True Value down based on the rent required to p

Small land area - I believe capital appreciation is predominantly in the land and properties with small land especially apartments, should have True Value adjusted down, however consider the location as well. Leasehold land should have the maximum adjustment downwards due to potential hikes in lease payments and lack of capital gains.

Reduced control - Shared driveways, flats, minor dwellings, body corporate involvement, cross lease sections, leasehold etc that reduce the autonomy of a property should be classified as risk. This certainly does not mean not to invest in these properties, just that they must have True Value downgraded.

Poor areas - Any area that you feel threatened or in danger then you should downgrade. I call it the stink eye test. If you drive through an area and you get stink eyes back to your smile then definitely adjust True Value down.

Areas in decline - For many reasons certain areas, cities or even countries can go through a period of decline. Properties may appear to be cheap but True Value should be adjusted down.

Every eight to ten years we experience a property boom. No-one ever seems to forsee the downturn but nonetheless investors should be prepared for tougher market conditions. Therefore, in an overheated property market adjust True Value down.

A note from Nick: It is critical to understand that the message is NOT to disqualify a property because one or more attributes would cause you to "adjust true value down", nor is Michael suggesting that you rush out and buy a home because several factors mean you adjust true value up. This is a tested framework you can use to analyse what a property is truly worth relative to where it is priced. The more you study and operate in a particular area the better you will become at analysing properties in this way.

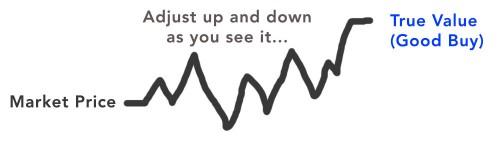

Here are a couple of pictures that illustrate this. Below you can see that if you adjust up and then down for whatever reasons but conclude that the True Value of a property is HIGHER than the market value then you should have more confidence that it is a good buy.

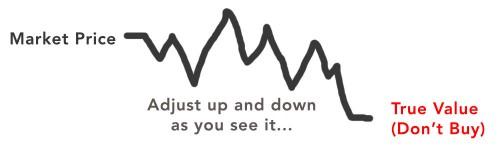

Here is how the opposite of that looks....

Summary

True value in your local area is simply Market Value plus or minus a factor which reflects a somewhat subjective value for present and future potential and costs. This adjustment of how YOU vision the property, the city and the economy in the future requires experience and education.

So what deals do you find? Well pull up a chair because we find a lot of very different properties for our wonderful clients, who (probably to their surprise) don't all want the same thing!

Read More…

.png)

.jpg)