by Nick Gentle on

Article appears under:

Investment Strategy,

About Property Investment,

Accounting and Tax,

Insurance,

Money Tips,

Mortgages,

The Numbers

by Nick Gentle on

Article appears under:

Investment Strategy,

About Property Investment,

Accounting and Tax,

Insurance,

Money Tips,

Mortgages,

The Numbers

The benefit of good knowledge or advice applied over time is infinitely more valuable than the cost.

Leverage means two things to me as an investor:

- Use other people's money to grow my wealth

- Us other people's time and skills to grow my wealth

I live by the idea. Just one valuable idea or skill, leveraged across a whole portfolio or business, is very powerful, and of course we need the bank's money to invest in real estate at all.

I believe in employing experts in my business regardless if that is mentoring, tax advice, property management, legal costs, building inspections, seminars, books, insurance advice, property finders (I've used them too, of course), architect/designer fees and getting expert advice on funding (mortgages).

If you learn to effectively master leverage you will enjoy financial abundance and security faster than you might have thought possible.

Be warned however, leverage cuts both ways and you want to make sure you utilize leverage smartly and carefully. This article outlines the rewards, and the risks, of leverage with property investment.

Leverage Other People's Money

The first form of leverage we learn about is using "Other People's Money" ("OPM") and when we think about leverage in finance the dictionary definition is:

Leverage: Use borrowed capital for (an investment), expecting the profits made to be greater than the interest payable.

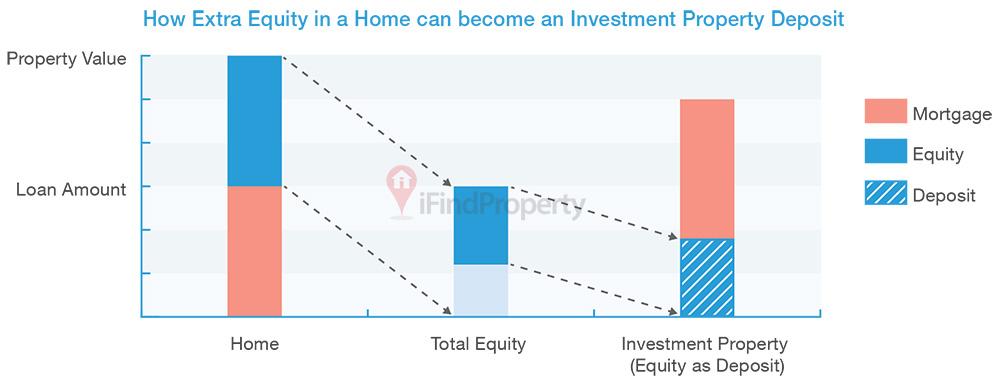

When you buy a property with a mortgage, you leverage the bank's money to buy an asset that is more expensive than you could buy with 100% cash. The strategy is of course that the income from the asset is more than the costs and you used that leverage to generate a profit.

It doesn't stop there, you also leverage your tenant's money to pay the ongoing costs associated with holding the property.

Capital growth is leverage working in our favour again. You receive all the increased value of your asset, however most of the money that went to buy and hold it came from elsewhere. Many property portfolios grow from investors using a capital gain as the on their next property.

It can be heady stuff and many investors once they work this out then run out to buy as many properties as they can. What investors do need to be aware of is the "deposit" in the right-hand bar above is also a mortgage. By borrowing again and again you can potentially become over leveraged and exposed to financial risk.

Important: The risks of becoming financially over-leveraged

As you grow your portfolio and your debt you become more exposed to changes in the economic landscape, such as interest rate increases, changes in bank or government policy, changes in economic fortunes of an area or unexpected costs.

If you don't have a sufficient cashflow and equity buffer and have simply borrowed more (because you can), then you can get into trouble.

Perhaps a story about two investors to illustrate; meet Peter and Paul.

Our two budding investors both get approval from the bank to buy their first rental property. Peter has been to a property investment course and since he wants to build a sizeable portfolio quickly and safely, he looks for a property where he can increase cashflow and value. Paul is focused on capital gains and is not concerned by cashflow.

Building a portfolio from leveraged gains is a common strategy, however make sure you understand the risks.

The market heats up and both soon find they have enough equity in their first property to buy another one.... then another. In two years they have 5 properties each.

Peter's properties return a higher yield because he realised that he was borrowing 100% each time and included cashflow and value-add in his criteria. He looked for properties where he could add value. Paul has also gained a lot of equity and indeed their portfolios are probably worth the same amount.

Paul might make a cashflow loss on each property but it is much smaller than his year-on-year equity gain, so he is not concerned and his accountant had talked about something called "negative gearing" as a tax strategy.

Then a recession hits. Interest rates are high and employment prospects low. The property market goes quiet and prices aren't being pushed higher and higher, rather, they come back a bit. The bank starts to get nervous because our two investors had expanded quickly and asks both Peter and Paul to both increase their equity position and shift some of their lending to P&I.

Peter is able to show a healthy equity buffer because of the value he had added and has no issue increasing his repayments.

Paul is unfortunately stuck because his properties already make a loss, and he doesn't have extra funds, with his job also at risk. He needs to sell a property to keep the bank happy. Unfortunately the market price is lower than what he paid for it so his position with the bank actually worsens and one after another he has to sell down his portfolio. Eventually he is left clinging to his original rental but with a higher mortgage than he started with, which he struggles to cover, looking at his high outgoings and no immediate sign of a turnaround he sells that property too in disgust.

Peter on the other hand is able to keep improving his position and once buying conditions eventually improve he's really able to accelerate.

Important side note to the important side note...

Interestingly had Paul stopped after buying his first property and quietly paid it off as most Kiwi investors do, he probably would have been perfectly fine, even with low cashflow. It was by "leveraging up" and increasing his exposure to market changes that he put himself in harm's way.

Leverage Other People's Time and Skills

Having a team around you is another form of leverage and while using "Other People's Time" (or "OPT") is not as sexy as "Other People's Money", it is equally important and this can be the differentiating factor for really successful investors, because not only can you buy more, but you can do more and usually do it better.

We (well, many of us) rely on our property manager and their team to find the right tenants, keep tenants happy and the building maintained, our broker or bank’s time to keep the loans in place, our accountant’s time to make sure our taxes are correct and up to date etc...

When the team around a deal is set up correctly, each person that plays a part will create more wealth for you over time than what they charge.

So, what about advice? The leverage potential of good advice properly applied is massive, simply because when applied to deals as expensive as property transactions the impact can be huge.

When the team around a deal is set up correctly, each person that plays a part will create more wealth for you over time than what they charge.

Tax and structures? One hour of a property accountant’s time to go through your goals and situation may cost you $200 - $300 but in return you have the most tax efficient and flexible structure for you. Restructuring down the line can cost thousands or tens of thousands in legal, bank and accounting fees, let alone any tax issues you may find yourself facing. The leveraged impact of good structure advice will become much more apparent when you have 5 properties, 15 years from now than when you are considering your first!

Whether you should pay for a mentor or coach gets debated a lot, with those who have done well under a mentor strong advocates and those who had a bad experience or figured it out on their own in the other camp.

Graeme Fowler wrote recently that it often takes the right student to get the most value out of coaching (or any advice really) and I agree with him 100%.

Like what you're reading? Register to get articles and investment property listings by email.

I am convinced that when we go into an education or advice situation with a specific goal to learn, we gain knowledge that when followed through upon, will make or save us tens or hundreds of thousands of dollars, if not millions.

Why so much? That knowledge is leveraged across our whole portfolio and every investment decision we make after that.

Case Study: Use Leverage to become Financially Free

I’ll share my own story a bit because it is a nice example of the power of leveraging a team of experts, the banks money and paying for the right advice.

I am convinced that when we go into an education or advice situation with a specific goal to learn, we gain knowledge that when followed through upon, will make or save us tens or hundreds of thousands of dollars, if not millions.

A few years ago now I had bought a rundown inner-city property through our at-the-time Wellington property finder and I wanted to remodel to increase cashflow, but I was stuck on how to best handle this. I was getting a lot of conflicting, albeit well-intentioned advice, for free. In the meantime, I hadn’t really focused on moving forward as an investor for a couple of years, so I was “scuffling”.

I signed up to work with a successful investor and coach who helped me work out the pros and cons of different approaches to my project. He in turn introduced me to an architect who understood the market I wanted to rent to and helped me find a good builder. I leveraged off their combined knowledge (and patience in answering all of my questions) and also my property manager in deciding on a renovation and remodel strategy.

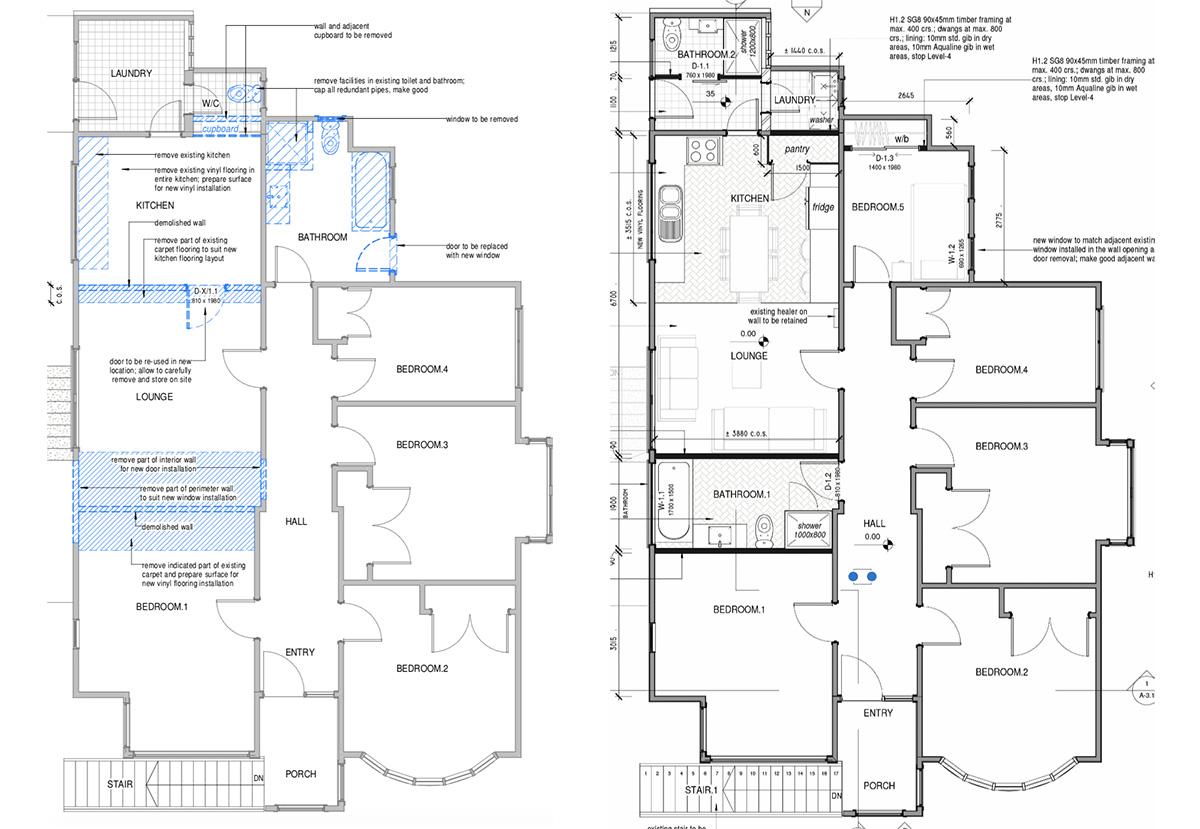

Before and after floor plans - more bedrooms, more bathrooms & better layout

The project added a bedroom and increased rent for all bedrooms (it is a student rental) so the value of the property went up by a lot. I thought that was good business and a lot of fun besides, so I sold some a property elsewhere and the proceeds and my equity gain from the above deal to buy a similar project, 9 months later and another renovation in the books I bought a third, which is ongoing.

In the grey box above I'm the one who added cashflow and equity as I expanded. The outcome has been life-changing financially but more than that I found that I really enjoy this style of investing. What many investors wouldn't want to touch with a barge pole (these projects take on average a year to complete), I am having a blast with and it is exciting that we are now helping other investors the same result.

Back to leverage. The most recent two deals I bought, planned and worked through largely on my own and while living in a different city. How? Well I co-run an investment property finding business (where clients leverage our knowledge to buy rental properties and get a team put together for team) so pulling together a team to make something happen is basically what I do. I worked with these folks:

- Property finder to find the deal

- An architect to look at potential configuration changes and advise on what would fly with council

- A builder to help appraise options and then of course later to do the build

- A property manager to advise on rent potential and more importantly “rentability” of different ideas

- A valuer to run the figures over with quickly

- A mortgage broker to secure funding for not only the house, but to pay for the renovation too

- An insurance broker to find a way to get both property cover and project works insurance during an insurance embargo. This is a whole separate article....

I was able to leverage their time and expertise to make it work and the bank's money to pay for it.

If I had stuck with what I knew and could control, none of this would have happened. I’d still be there with my first property trying to figure out what to do with it.

The good news is you don’t need to be at the renovation/remodel extreme end of property investment to reap the benefits of leveraging a great team. Nor is it only for people who plan to build a large portfolio.

It doesn’t matter if your style of investing is “set and forget”, new build, “roll up your sleeves” or something else. The benefits of getting the right advice, funding and help at the right time (and acting on it) will compound exponentially over time for any investor.

Nick Gentle

Business Owner & Operations Manager

nick@ifindproperty.co.nz

027 358 3855

.jpg)